First They Blocked Payments to a Palestinian Children’s Centre & then Lied & Blamed it on Government Sanctions

When I Complained About Their Racist Discrimination They Told Me That

They Were Closing My Accounts!

When people think of Building Societies they think

of what is the fluffier side of British financial institutions. Most building

societies like the Woolwich, Halifax and the ill-fated Northern Rock demutualised

and became private banks in the 1990s and 2000s.

Most of them were subsequently taken over by the big

banks or nationalised in the financial crash of 2008/9. Nationwide emerged as the largest of the remaining building

societies.

Today it is clear, with its acquisition

of Virgin Money for £2.9 billion, that Nationwide

aims to be one of the big banks. It has also removed

the accounts of critics of its expansion plans, so I am not the only casualty

of its aversion to free speech. Despite having members’ AGMs building societies

are anything but democratic. The same old Establishment worms its way in along

with their amoral culture.

My problems with Nationwide

began on February 2 and 12 when I sent £2,000 and then £1,500 to the

Al Tafawk Children’s Centre in Jenin. Little did I know that 4 months later it

would end up with me being told that they were closing my accounts. I’ve been

with Nationwide for 25 years but that

counts for nothing.

The first indication that something was

amiss was when I received 2 emails from the Accounts Review Team [ART] (9 &

12.2.24) asking:

• Why is this payment is

being sent via your personal account, on behalf of The Brighton Trust, and not

directly from the registered charity’s own bank account? Will this payment be a

one-off or an ongoing arrangement?

• We require evidence

that beneficiary account details are associated to Al Tafawk Centre.

On 13 May Hannah from ART rang me and we

had a perfectly pleasant conversation. Hannah told me she was happy with my

responses. After we spoke I emailed her to confirm the details of our

conversation. My email began:

Good to talk to you and glad we

have resolved this though I am really unhappy that it was because of a payment

to a Palestinian NGO. I'm sure that this would not have happened with an

Israeli Children's Centre.

If as I suspect your concern was

that we might be funding 'terrorism' then I can lay your concerns to rest. Our

charity only funds a children's centre - it used to be toys and equipment but

today water and food is the priority

Clearly I trod on some raw nerves as the ART clammed

up. Hannah didn’t reply. They also failed, until 5 March, to recredit my

account with the money that they had refused to transfer. For a month I could

get no explanation as to what had happened to the money and whether it had been

sent on as Hannah had promised.

I made a complaint about their behaviour and Louise from

Member Service ‘investigated’ my complaint and found nothing amiss. At which

point I protested at her barely literate, contradictory letter and demanded a

proper investigation. I began my appeal thus:

In her letter to me of 20 February Louise Morris

stated that: ‘I hope this letter explains

things clearly’ and goes on to say that ‘If

you think I’ve missed anything... please email me. Clearly Ms Morris has a

sense of humour.

My appeal was

upheld on 6 March by Simon, a Team Manager at Member Service and I was awarded

£250 compensation. My complaint concerned the behaviour of the ART. I

emphasised, once again, that this would not have happened if I’d tried to send

money to an Israeli children’s centre.

On 7 March I

sent an email to the ART asking a simple question viz. ‘Will you hold up future payments? I went on to say that

‘your

discrimination against a Palestinian children's centre is an outrageous example

of racism as this would not happen in the case of Israel. Presumably Jewish

children are kosher and Palestinian children are not.

The latter remark

was humorous but I suspect that a sense of humour is something that is alien to

the Israel’s supporters in the ART.

On

26 March I received a ‘Final Warning’ from Haleema, a Member Relations

Consultant (!) which began:

‘I've

been told that on 07 March 2024, you sent our Review Team emails consisting of

abusive and racial comments. This type of behaviour goes against our account's

terms and conditions and we won't put up with it.

My first

reaction to this letter was to wonder whether Member Service employees have any

training. If Haleema was minded to issue me with a final warning (it was the

first!!) she might have bothered to read the email she was commenting on. Or is

it general practice for Nationwide

staff to accept allegations at face value?

The email in

question contained nothing abusive or ‘racial’ (unless a reference to Israel is

considered ‘racial’). Clearly this letter had been cooked up behind the scenes

and was the product of a ‘revenge complaint’ from the ART at having had an

adverse finding made against it.

I attempted to

resolve matters informally with Haleema but she didn’t comprehend the points I

was making. As a result, on 5 May, I made a complaint.

On

21 May I chased up the complaint and on 23 May I received a letter turning down

my complaint from Rhianna. She too seemed to have difficulty reading but whereas

Haleema had accused me of sending abusive emails Rhiannon changed this to a question

of perception. The problem was that:

I appealed this and on 19 June Fay

Ingram asserted that

I

called the Israeli army ‘bastards’ which is descriptive not swearing. The phone

call in question was terminated when I challenged the staff member as to why no

information could be provided about my funds.

But

it’s not clear why that should cause upset. It’s simply a comment unless of

course members of ART have some form of emotional attachment to Israel’s genocidal

army.

I

also emailed a number of people about what had happened to me and they wrote to

Nationwide. It is clear that Nationwide actively discriminates

against sending payments to Palestinians.

This

is especially shocking given that Israel’s illegal occupation of the West Bank

openly flouts the 4th

Geneva Convention relating to the protection of civilians

at time of war. The International Court of Justice at The Hague has just ruled

that Israel’s occupation of the West Bank is illegal. Yet despite this Nationwide is refusing to transfer money

to Palestinians on the West Bank whilst placing no obstacles in the way of

transfers to Israel’s settlers.

In a letter to Mr T on 8 May Nationwide wrote:

we’re

unable to send monies to countries currently under sanction by the UK

government... we regrettably cannot make

transfers to countries on the high-risk list... We’ve to abide by this list and

cannot give any more information on why we cannot send to this relevant

country.

The relevant

country in question was Palestine. Then on 17 July Andrea Doyle wrote a second

letter apologising for the ‘confusion’ that their first letter caused. Doyle

wrote:

Within our response we noted

that payments cannot be made to any countries that are sanctioned by the UK

Government. Given the context of your letter, you may have understood our

letter to be suggesting that Palestine is a sanctioned country. I apologise for

the confusion this appears to have caused. To clarify, Palestine is not a

sanctioned country under the UK Law.

... we do

occasionally need to stop payments and seek further information about the

nature/purpose of the payment. In some instances, again in order to comply with

our obligations, we do need to refuse payments. However, such decisions won’t

have been based on the fact that the payment was being made to an unsanctioned

or non-proscribed organisation operating in Palestine.

Describing

Palestinian organisations as ‘unsanctioned’ or ‘non-proscribed’ casts a pall of

suspicion and guilt over them. Would Israeli organisations be so described?

This

letter was disingenuous. There was no confusion. The first letter made it clear

that Palestine was subject to sanctions. That was wrong. Why not admit you were

wrong?

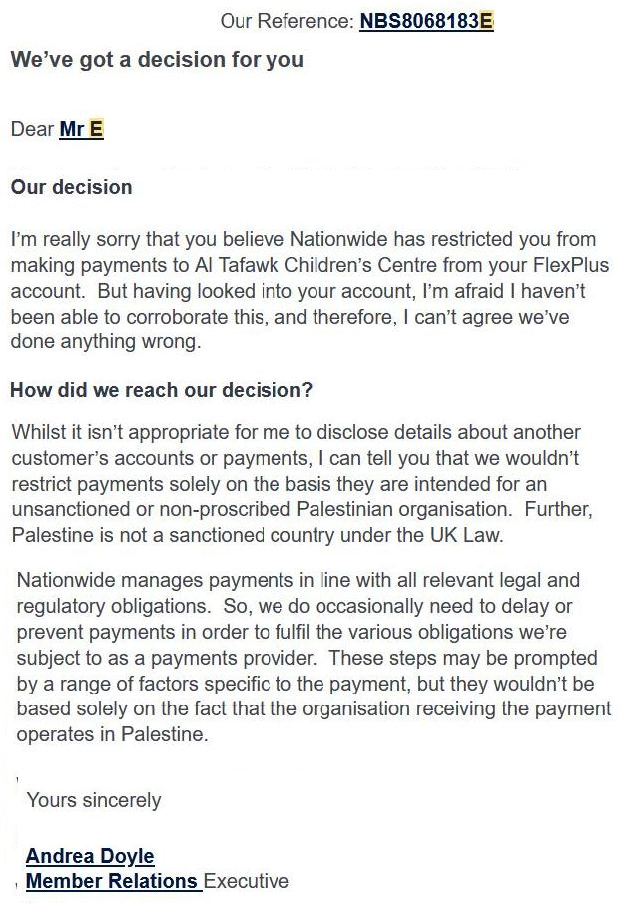

In

an email to David, also of 17 July, Doyle wrote that:

I can tell you

that we wouldn’t restrict payments solely

on the basis that they are intended for an unsanctioned or non-proscribed

Palestinian organisation. (my emphasis)

Identical

comments were emailed to Mrs E, Mr R, Mr W, Ms M, Mr B, Mr R, Mr W, Ms D Ms R – all on 17 July by Andrea Doyle

and in one case Emily Draper. Note the word ‘solely’. In other words if you are

trying to send money to Palestine, a country the subject of an illegal occupation,

it may not be the only factor in a refusal to transfer money but it is clearly

a major if not principal factor.

It is clear that Nationwide is

in practice refusing to make payments to Palestine. Why? Well one can only

assume that members of the ART sympathise with Israel’s military and therefore

took exception to me criticising the ‘world’s most moral army’ as bastards!

This was expressed in a letter of 23 May by Rhiannon which stated

The hypocrisy of this beggars belief. It is the behaviour of the Three Wise Monkeys

who refused to see, hear or speak evil.

The reason that the ‘conflict’, in fact occupation of Palestine by

Israel, was raised was because Nationwide

refused to transfer payments to a Palestinian children’s centre. It was they

who allowed the situation in the Middle East to intrude on their decisions. Nationwide took and still takes a

position that anything Palestinian is suspect. This is confirmed by the letter which

has been issued which says that being Palestinian won’t be the ‘sole’ reason for refusing transfers.

In her email to me of 19 June, Fay Ingram, asserted that the ART

‘doesn’t have to answer specific questions about a block that has

been placed’ and ‘that we actively review all payments and can stop payments when we

hold concerns.

Of course the ART doesn’t have to answer questions but what

possible reason can there be for not doing so? It is a lie that they ‘actively review all payments’. Over

time I’ve made a number of international payments from Nationwide. They have never been

subject to any hold-up. These are camouflage words.

This is especially relevant when the ART provide a false explanation

to another customer about Palestine being a sanctioned state.

However much Nationwide

twist and turn it is clear that in practice they are operating a policy of

sanctioning Palestine. When I’ve tried to send money from other banks I haven’t

had this problem. If Nationwide is to

maintain that it’s not treating payments to Palestine differently then it needs

to challenge the anti-Palestinian racism which permeates the ART. They should lay

down clear rules and guidelines about not discriminating against the Palestinians

whose only crime is suffering under an illegal and brutal occupation.

I have quoted only brief excerpts from the email correspondence.

If you wish to see the full emails, then they are saved here.

One final matter. The first time I learnt that my accounts were being closed was on 24 June when I receive a ‘reminder’ that my accounts were being closed. I had not previously had any such notice although Nationwide maintains that a letter was sent out on May 10. Given my post is reliable my suspicion is that this letter was never sent.

What is interesting is that on 19 June, over a month after the

letter of May 10 was apparently sent, Fay Ingram wrote to me stating that

Why was Ingram saying that my

accounts could be closed when

elsewhere Nationwide are asserting

that such a decision had already been made?

Likewise Rhiannon sent an email on

23 May saying of Haleema’s letter that ‘I can’t agree that we...

threatened we’d close your accounts.’ She

may not agree but how else should I interpret Haleema’s threat that

if

we hear about any further incidents or similar behaviour towards our

colleagues, we'll close your account immediately without telling you first. [bold in

the original]

Rhiannon’s email was sent nearly a fortnight after the letter

closing my accounts was apparently sent. It reveals how shallow Nationwide investigations are that they

are unable read their own correspondence.

It is clear from my recent

experiences with Nationwide that

their attitude to Israel/Palestine is that of the Britain’s Political Establishment

which is to penalise the Palestinians and treat Israel as a normal western

democracy. This means ignoring the fact that Israel is illegally occupying Palestinian

land and adopting a mentality that conflates Palestinians with terrorism and

sanctions.

What You Can Do?

Although

some people have written threatening to close their accounts if Nationwide doesn’t change their stance

I’m not asking people to do this. Nationwide’s

institutional racism and amorality is par for the course in the capitalist

banking world.

What

you can do is to bombard them with complaints about their behaviour and demand

accountability for decisions to stop transfers to Palestinian organisations

such as children’s centres. This is especially the case if you are a member.

Tony

Greenstein

Disgusting behaviour from Nationwide. I have my own reasons for never banking with them again.

ReplyDeleteI worked for them for quite some time as a consultant to the BoD and some of their behaviour then...particular the senior executives...was disgusting. If I shared some of the things I came across, customers would be closing their accounts regardless of Palestine.

ReplyDeleteI worked for them for quite some time as a consultant to the BoD and some of their behaviour then...particular the senior executives...was disgusting. If I shared some of the things I came across, customers would be closing their accounts regardless of Palestine.

ReplyDeleteThis is Zionism, disgusting

ReplyDeleteThis is Zionism, disgusting

ReplyDeleteAre they bothered about my feelings as a muslim now they cant deny israeli apartheid and genocide.

ReplyDeleteIf not surprising, this behaviour is fundamentally regrettable (said also as an account holder). It looks like the Society filters certain transactions through a shadowy template prejudicial to charities precariously assisting those in the most extreme distress.

ReplyDeleteAlthough initially seeming to be dealing with the crux of the matter, the Nationwide's subsequent handling appears unambiguously political and to infer a suspect motivation on the part of the account holder. The Society's £250 compensation payment underlines such an interpretation.

What Can Be Done ?

It is only fair to say that the outlook of this 'ART' is typical of the financial services sector in general, but that's not to imply that (i) the response of the Nationwide BS to the substance of Tony's complaint has been adequate in declaring its motives, nor (ii) that its customers should passively have to be implicated in its conduct. It's our money. I'd like to see what reply is forthcoming to Judy's request (above) of 16 July 2024. Regardless, their ART is in dire need of some professional development tuition.

On the one hand ...

In the light of the ICJ's Opinion of 19 July last, the Nationwide might want to revise its attitude. The Society might elect, once persuaded to review its stance, openly to CONFIRM the robustness of remittances sent to Al Tafawk via its branches, even perhaps consider a modest donation itself in respect of the potential negative publicity that attaches to its prior actions, which will have interrupted the charity's critical work.

.. while on the other:

There are a couple of avenues to explore, depending on how much of a price one might want to try to attach to the obstructiveness of the Nationwide's behaviour:

- If a complaint has not been satisfactorily handled by a financial institution, it may then be referred to the FCA for resolution, the outcome of which referral can result in compensation for the complainant and fines for the institution. Takes time and patience, of course, but could be significant in the aggregate in stopping banks/BSs frustrating legitimate transfers in this way.

- Reduction of one's holdings with the Society, especially if there's a credit card attaching to an account, to create a perpetual negative periodic balance of funds, interest-free (i.e. minimally maintained current account surplus, but settling the card account in full JIT every month from funds held elsewhere). Stealthy and vindictive perhaps, but they started that ;).

The above apart, it is dumb PR to risk any kind of complicity with apartheid regimes, as the indelible stench attaching to Barclays over the decades demonstrates.

Sorry to hear about this. I have been with Nationwide for a long time. I called them and have registered a complaint about how this has been dealt with.

ReplyDeleteNationwide management have become too big for their boots. I will close my account as soon in the near future.

ReplyDelete